When it comes to value investing, most Wall Streeters try to bend the reality of an otherwise more straightforward existence; guiding you through the jungle of finding above-market returns seems more lucrative than simply educating you on the factors that make a good deal.

There is a fresh new list out there, composed of the hottest value deals today, which - so far so good - check out all the significant metrics value investing legends look for when sourcing their next considerable investment.

Through this list, you, too, can beat the market over the long term and even find yourself holding some of these names longer than you may think, which can significantly - depending on where you live - reduce your tax burden at the time of sale; you know, the whole short-term versus long-term gains tax.

Williams Sonoma

Do not look at this chart just yet because it will start to look a lot like Bitcoin during the last crypto boom and bust. Rest assured, Williams-Sonoma (NYSE: WSM) has more steam behind its momentum than just market hype; it's time to break down this value deal.

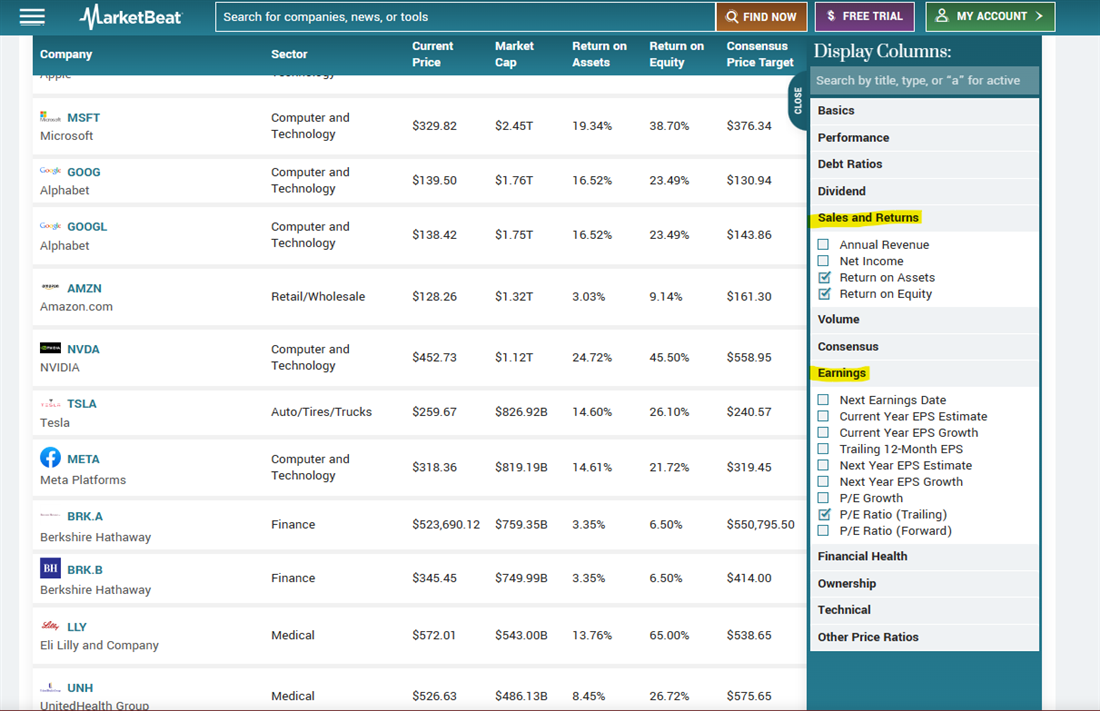

As part of the consumer stocks universe, Williams-Sonoma stands out; how? Lucky for you, MarketBeat offers a fantastic filtering tool to spot the needle in the haystack.

With the stock screener, you can add a return metric that reads "Return on Assets" and another "Return on Equity" to find the most profitable stocks in a given sector.

As shown in the image above, filtering by profitability and price can lead you to find high-quality assets at a relative discount, the foundation of value investing. The question is, does Williams-Sonoma fit?

On a five-year average basis, the financials will reflect an ROIC (return on invested capital) of 28%, which is massive for a company in this sector. ROIC is essential because, over the long term, annual stock price performance tends to mimic the percentages seen in ROIC.

What about the rest of the business fundamentals? The company sports a gross margin consistently above 35%, implying some pricing power moat and excellent relationships with suppliers despite current supply chain issues.

Moreover, according to the company's latest quarterly earnings, management has bought over 4 million shares from the open market. If insiders believe the stock to be cheap enough to buy, shouldn't you? Well, it's more complicated.

Without getting lost in the weeds, you can compare today's 11.0x P/E ratio to the historical record, showing a pre-pandemic valuation of 18.0x to 20.0x. In this case, management is doing right by shareholders through buying back cheap shares.

Buckle

Hovering near its 52-week low price and sporting most - if not all - of the metrics investors look for in a value deal, Buckle (NYSE: BKE) is a straightforward study case to add to your arsenal.

Analysts support the future of this stock as they come together to agree on a $38.0 share price target, implying a 16.6% upside from today's prices.

It's time to go through the vital sign checklist and give these analysts a run for their money, starting with ROIC and some of the main margins. Over the past five years, financials will show an above 25% ROIC, check for above-average compounding returns opportunity.

Buckle showcases a steady 55% plus level on a gross profit basis, which is almost unheard of for a retail stock. Whether it's brand penetration or superior quality, this company is pumping out a product that the market cannot get enough of, or so the numbers imply.

The same trends extend to net income margins, which come in above 14% year after year, another tremendous achievement for a clear industry outlier. Now that you've spotted the initial signs of a potential value investment, it is time to check the price tag side of the equation.

Low P/E stocks are typically considered to be trading below a 10.0x multiple. In the case of Buckle, a 6.8x P/E will not only make it cheap today but place it at its lowest valuation since the troughs of COVID-19.

But wait, there's more: if buying a falling stock is too much for your gut, management is here for you. This stock offers a 4.3% dividend yield to cushion your wait time and beat inflation while at it.

H&R Block

There are only two things that will be certain for every homo sapiens on this planet, death, and taxes. Playing on this incredibly robust moat of inevitability, H&R Block (NYSE: HRB) makes for a tremendous opportunity at the right price.

Accounting and tax reporting are two things that have mostly stayed the same since their inception, which is why the slightest touch of technology can act as a significant disruption, and H&R knows this.

Spruce, the mobile banking platform launched in June of 2023, has already drawn over 300 thousand users, boosting growth and revenue opportunities for the firm. But how does the checklist play out for this one?

ROIC stands at a five-year average of roughly 20%; again, it is an excellent rate to put your hard-earned dollars to work. Gross profit margins above 44% and net income margins above 15% will aid in the further growth of each invested dollar in the not-so-distant future.

What's the price? Management has already repurchased up to $500 million worth of stock, which makes sense considering it is trading at a 10.0x P/E, significantly below its pre-pandemic valuation of 15.0x to 17.0x.